731/Getty(2)

‘Hey, Hey, Money Maker’: Inside the $156 Billion SPAC Bubble

This Wall Street craze is stretching all the limits and involves flying taxis, bikini GIFs and a rapper with a taste for champagne.

Whenever greed meets reality and giddy markets collapse, Wall Street pros usually admit that they sensed the end was coming. The warning signs were so familiar, they belatedly confess, that it was difficult to believe anyone could miss them. The chain of fools was running out.

This can’t last. Today those sober words are being whispered again in American finance, this time about one of the biggest money-grabs in the business, SPACs.

Who hasn’t heard about SPACs by now? Once dismissed as sketchy Wall Street arcana, these publicly traded shells are created for one purpose: to merge with real businesses that actually make money. Nowadays everyone who’s anyone seems to be doing one. Sports figures like Alex Rodriguez and Shaquille O’Neal; former House speaker Paul Ryan; Wall Street rainmakers like Michael Klein — the list runs on. The count from the past 15 months stretches to 474 SPACs. Together, they’ve raised $156 billion.

Picture GameStop Redditor meets “Wolf of Wall Street,” and you get the idea. The celebrity-studded spectacle will either prove that SPACs — officially, special purpose acquisition companies — are transforming the way finance gets done, or that the market mania is spiraling out of control. Maybe both.

Privately, and increasingly publicly, financial professionals warn this will end badly for the investing public. To cynics, the only questions are when, and how badly. More and more members of the SPAC ecosystem — a matrix of hedge funders, private-equity dealmakers, bankers, lawyers and assorted promoters — see the excesses building. They point to you’ve-got-to-be-joking valuations, questionable disclosures and, most worrisome, a growing misalignment of interests.

On one side of the divide are the people minting SPACs and getting rich now. On the other side are the people buying into SPACs and hoping to get rich later. The Securities and Exchange Commission has been running up red flags.

The bad omens are all around. I called a private-equity executive who was eyeballing a list of 20-or-so SPACs, a mere week’s worth at the time. He figured five might be worth investing in. Rodriguez, the baseball-shortstop-turned-entrepreneur, recently told Bloomberg Television that his goal was to build “the Yankees of SPACs.” The real estate billionaire Barry Sternlicht mused that a member of his domestic staff — his “very talented house manager” — probably could pull one off too. An analyst at a major bank told me he’s thinking about doing a SPAC. He asked, half-joking, if I wanted in.

“It’s just so easy,” he told me.

Cassius Cuvée is among the believers. He’s a hip-hop artist and self-professed cannabis and champagne enthusiast from Oakland, California. A friend turned him on to SPACs after the fantasy-sports site DraftKings Inc. stormed into the stock market with one, clearing the way for Richard Branson’s space-tourism company, electric-vehicle startup Nikola Corp. and the rest. Cuvée was so taken by the money that he laid down a track, “SPAC Dream.” His song made the front page of the Wall Street Journal. Its lyrics capture the mood:

I’m like a SPAC

What the hell’s that?

You get in on the ground floor

It paid big

So searched and then I found more…

“I’ve done better than I ever thought I would,” says Cuvée, who claims he’s got about $500,000 invested in 40 or 50 different SPACs. He took some lumps at first but brushed up by watching TV and scrolling Twitter. “Now I know what I’m doing,” he says.

How did we get here? Short answer: slowly, and then all at once. SPACs first emerged in the 1980s and for a long time were relegated to the pink sheets, where penny stocks lurk. Until recently, they were viewed mostly as a last resort for dealmakers looking to raise money.

The Covid-19 pandemic changed all that, as it has so many things. On today’s work-from-home Wall Street, traditional roadshows — those traveling, if-it’s-Tuesday-it-must-be-Dallas sales pitches for new stocks and bonds — have become scarce. Rock-bottom interest rates have fueled the historic “everything rally” in equities, Bitcoin, what have you. Propelled by greed and boredom, millions of amateur investors, cheered on by social media, have piled into meme stocks like GameStop — and SPACs.

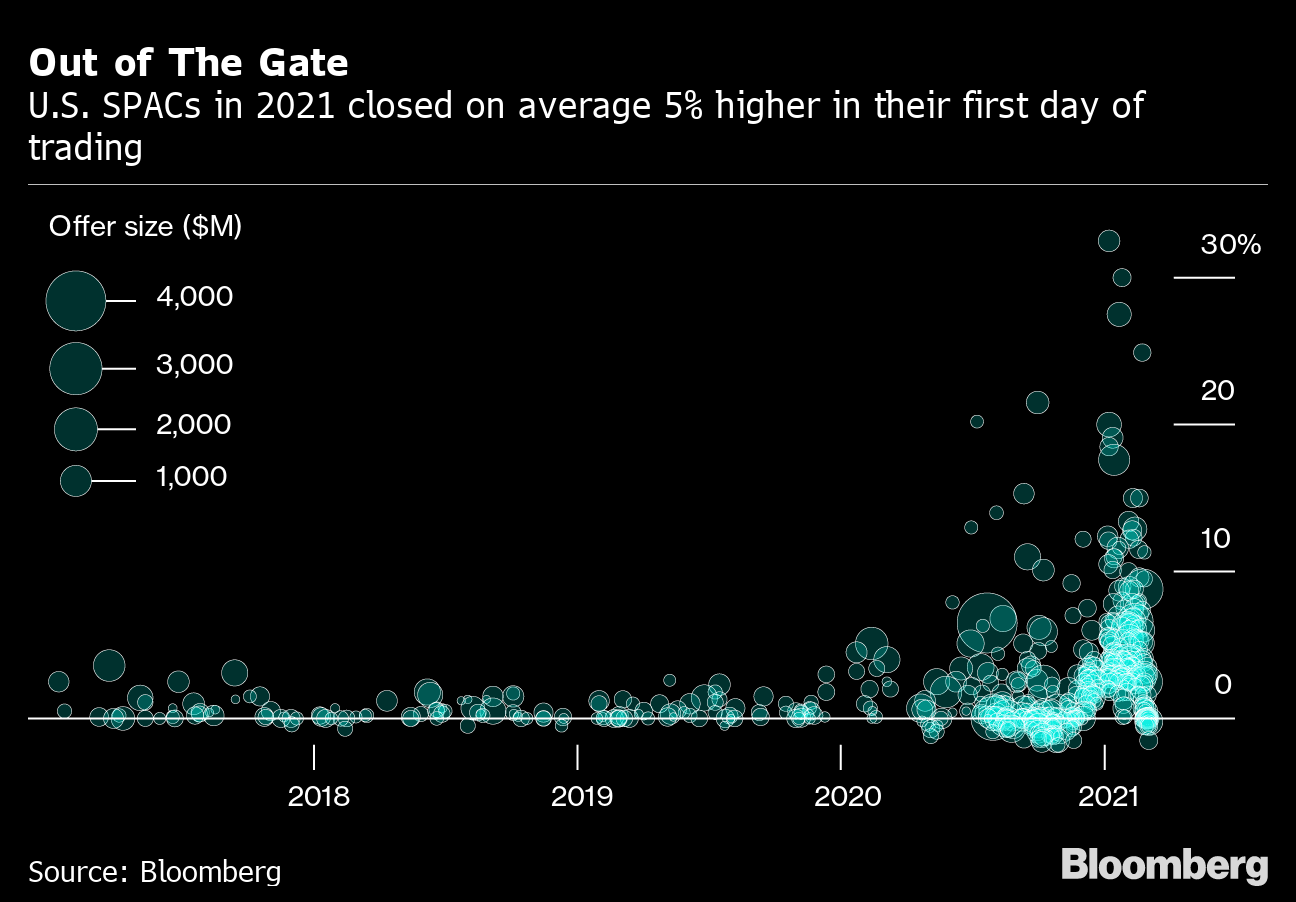

The numbers tell the story. In 2019, 59 SPACs raised $13.6 billion. In 2020, those figures leaped to 248 and $83.3 billion. So far this year, the totals are already at 226 SPACs and almost $73 billion, with SPACs making up more than 70% of the IPO market. Along the way, prominent financial players like Apollo Global Management Inc. and KKR & Co. have lent SPACs the legitimacy they long lacked.

Naturally, SPACs that can find great private companies to buy will pay off for all concerned. They typically have two years to pull off a deal and enable businesses to bypass the laborious, details-heavy process of reaching the stock market via old-fashioned initial public offerings. Among the biggest of late: electric-vehicle maker Lucid Motors Inc., which, amid much hoopla on Reddit, merged with a SPAC founded by Klein. The combined value at the time quickly rose to roughly $57 billion — bigger than Ford Motor Co.

The dangers are the usual ones, whether the investments in question are meme stocks, dotcoms, subprime mortgages or tulip bulbs: greed and hubris. Fund managers say some SPACs are betting on companies that not long ago were struggling to raise money from risk-loving private investors. It’s become a sellers’ market: some businesses are going from one SPAC to another, shopping for better terms. Bankers have a term for the play: a SPAC-off.

“People have made a ton of money, and they don’t realize it’s not sustainable,” says Sahm Adrangi, founder and chief investment officer at Kerrisdale Capital Management, a New York-based hedge fund that makes short bets against companies, including SPACs.

The aircraft stands poised, six black propellers turned skyward, gauzy light glinting off its silvery skin. Twin-tailed and blimp-shaped, it might look at home in a galaxy far, far away, in the “Star Wars” universe.

For now, from a business perspective, it’s about as real as a Jedi.

The futuristic electric craft — or at least the artist rendering of it on the internet — is the brainchild of a young company called Archer Aviation. Its plan is to build helicopter-type vehicles that can whisk passengers quickly and quietly above Earth-bound traffic for the price of a $50 Uber. “The flight of a lifetime, every day,” its website promises.

A money manager at a brand-name investment firm told me that Archer came to him last year looking for private financing. He passed. In fact, he didn’t even take a meeting. As he pulled up a PowerPoint outlining the proposal, he remembered why: to him, the company looked more like a science project than a business.

Such skepticism aside, Archer Aviation nonetheless has managed to land on the venerable New York Stock Exchange as if it were a Boeing or Airbus. It got there via a SPAC orchestrated by Ken Moelis, another prominent dealmaker, who has started to raise money for three other SPACs.

Archer’s good fortune is a testament to SPACs, also known as blank-check companies. SPACs have a lot of wiggle room in valuing the businesses they buy. Unlike traditional IPOs, where financial results are in focus, SPACs can base entire deals on projections.

When I reached out, a spokeswoman for Archer said it’s been testing an 80%-to-scale prototype at private airfields in California. It hasn’t carried pilots or passengers. The company says it will turn out 500 flying taxis by 2026. United Airlines has promised to buy at least 200, provided a range of conditions are met, to spirit passengers from Hollywood to Los Angeles International Airport. Archer says it’s the only company in its space — that is, electric vertical takeoff and landing aircraft, or eVOTL — that has secured a commercial contract for orders. It also has a major auto manufacturing partner with plans to make electric cars.

That, essentially, is enough for a SPAC.

The math is jaw-dropping. Only last April, a round of seed funding valued Archer at $16 million. Moelis’s deal has placed a higher value on the company: $3.8 billion. In other words, in less than a year, the valuation has jumped 23,650%.

“There are a significant number of SPACs betting on concepts, rather than looking at real and projectable revenues,” Mark Attanasio, co-founder of the $30 billion Crescent Capital Group and principal owner of the Milwaukee Brewers, said of SPACs broadly. Crescent, naturally, has a SPAC too.

A woman in a navy blue thong-bikini swims by in slow motion, her derriere framed amid a swirl of bubbles. The subject of this GIF and accompanying Twitter post: Lucid Motors, the would-be Tesla of the SPAC world.

“This stock gives me a hard-on,” wrote the anonymous poster, who goes by the handle Dr. SPAC. “Am I allowed to say that?”

Dr. SPAC’s Twitter feed is one of countless social-media accounts fueling the SPAC boom. Many have tens of thousands of followers. Dr. SPAC has 28,000.

Dr. SPAC’s avatar is three cartoon-ish money bags. His profile says he’s an experienced investor with over 20 years in the business. It adds that his posts are “for entertainment purposes only.”

Among Dr. SPAC’s fans is the hip-hop artist Cuvée, who celebrates some of the popular new SPAC-centric voices in “SPAC Dream”:

I followed Dr. SPAC and SPACWatch

I see yeah...

The field also includes SPAC Tiger, SPAC Guru, SPACzilla and Bill SPACman (a nod to the billionaire investor Bill Ackman, whose new SPAC has gained 30% percent while still searching out a deal).

I direct-messaged SPAC Guru, asking to talk. He got back in one minute.

Six months ago, SPAC Guru told me, he had one follower on Twitter. Now, he has more than 75,000. He declined to divulge his identity, saying people on the internet can be crazy and unpredictable. He did say he was a retired investment banker and spends his days at a desk with nine screens, managing money for himself, his elderly mother and his teenage son. He drums up interest in SPACs by directing followers to everything from regulatory filings to Harvard Law Review articles.

SPAC Guru said he’s had followers tell him they’ve made enough money from SPACs to pay off their mortgages, dig out from under credit-card debt or put a family member through college.

“When the sun is out, you make hay,” SPAC Guru told me.

Exuberance aside, the history of SPACs isn’t on the side of the investing public. According to Bain & Co., 60% of SPACs that acquired businesses between 2016 and 2020 have lagged the fast-rising S&P 500. As of late January, about 40% of these SPACs were trading below their starting prices.

Some SPACs have fared better — much, much better. DraftKings, which turned Cassius Cuvée’s head, has soared almost 450% since its SPAC deal was announced in late 2019.

Out of The Gate

U.S. SPACs in 2021 closed on average 5% higher in their first day of trading

Source: Bloomberg

Another, backed by billionaire Tilman Fertitta and Wall Street grandee Richard Handler, similarly crashed after acquiring Waitr, a would-be Grubhub Inc. The result has been a class-action lawsuit. No one in the SPAC game thinks this suit will be the last.

However acquisitions actually pan out, the odds favor SPAC sponsors and their Wall Street enablers. Sponsors typically collect a 20% bounty, known in the trade as the “promote,” as well as other perks that help minimize their downside.

Take Lucid, the EV startup. As part of its SPAC deal, Klein and his partners received 51.75 million shares, and bought 42.85 million warrants at $1 a piece. At going market prices, their stock is worth about $1.26 billion. They stand to make $553 million more on the warrants.

Enthusiasm was so high that several big investors told me they had to decide within a day whether to put money down or not, with no chance for the usual follow-up questions. No sooner did Lucid confirm its deal than the company announced its first model would be delayed until the second half of 2021. The stock promptly swooned.

Klein, for his part, just finished raising his seventh SPAC. He didn’t return telephone calls seeking comment.

“The economic incentives for serial SPAC sponsors are that if they win one and lose one, they usually still win,” Crescent’s Attanasio says of the industry.

The economics are also good for Wall Street banks. They collect lucrative fees for advising SPACs, providing still more incentive to keep the SPAC game going. Citigroup, for instance, has collected about $200 million in recent years for advising on various Klein SPACs.

Only a year ago, as the pandemic roiled world markets, shut down economies and emptied skyscrapers in New York, London and Hong Kong, few would have predicted that SPACs would explode. Today, many sense the jig will soon be up — that time is running out.

The SEC has been making noises about SPACs for months now. After warning about potential problems in September, the agency came back in December with new guidance for clarifying potential conflicts and exactly how much money SPAC sponsors stand to make.

“The rapid increase in the volume of SPACs represents a significant change, and we are taking a hard look at the disclosures and other structural issues surrounding SPACs,” said John Coates, acting director of the agency’s Division of Corporation Finance.

Sober-minded bankers foresee this end:

In 12 or 18 months, as today’s crop of SPACs approaches the end of its 24-month lifecycle, some founders will stretch for acquisitions rather than hand money back to investors. Having to lock down deals, whatever the terms, will bring an end to the days of easy money. Eventually, much of the market will be washed out.

“In the rush to get deals done, you hate to say this, but people will cut corners on due diligence,” Greg Belinfanti, an executive at One Equity Partners, said at a recent Bloomberg New Voices virtual event.

Many SPAC buffs predict a kind of Biblical deluge, with an Ark only big enough for Wall Street A-listers. SPACs, many say, will once again fade into the background, overshadowed by IPOs or whatever shiny new thing comes along.

“Whatever stops this bull market will lay its first sights on SPACs,” says Steven Siesser, a partner with law firm Lowenstein Sandler. “They'll be the first casualty.”

Until then, Cassius Cuvée will keep rapping the SPAC anthem:

See me chasin’ paper,

I’m a money maker

See me chasin’ paper,

I’m a money maker

See me chasin’ paper,

I’m a money maker

Hey, hey, money maker

Money maker

Money maker

Money maker

— With assistance by Pratish Narayanan, Tom Maloney, and Crystal Tse