With less than six weeks away from the Tesla (TSLA) Model 3 finishing off its first year of production, you are just as likely to find a unicorn as you are the base $35,000 version. Given how much importance this vehicle gets when looking at Tesla's future, I'm here today to discuss why not delivering at this price anytime soon will only make the situation worse.

Musk's latest tweet is another contradiction:

When the Model 3 was unveiled in March 2016, hundreds of thousands of deposits were soon placed for the vehicle. A lot of buyers were interested in the starting price point, $35,000, and nearly 26 months later they are still waiting. Recently, CEO Elon Musk was asked on Twitter regarding the timeline for this version, and his reply is seen below.

(Source: electrek article, seen here)

(Source: electrek article, seen here)

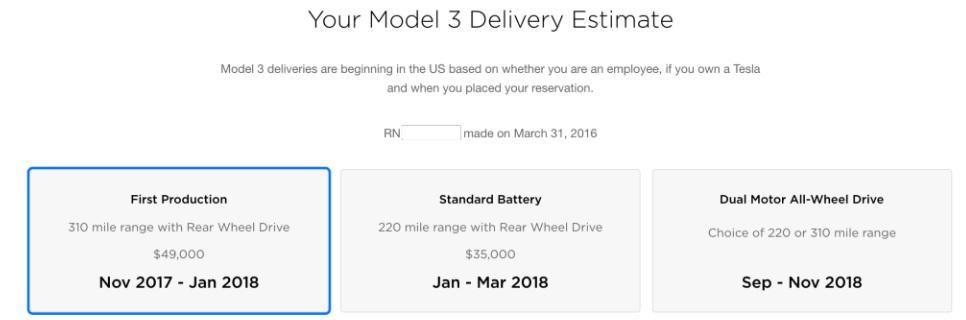

Part of the bear case is that Tesla cannot deliver the base model and make a ton of money, which seems rather obvious. As we've seen with the Model S and X, Tesla needs to sell more higher end versions for gross margins to be somewhat adequate, and that's before all of the spending on R&D, SG&A, etc. But to make my main point, let's go back to the July 2017 Model 3 timeline, something I posted in a Tesla article last year.

At that time, Tesla was planning on getting to 5,000 units of production a week by the end of 2017, which meant that deliveries would start immediately after. Now, Elon seems to be saying they need 3-6 months after hitting that level to get there, meaning the original timeline was extremely optimistic. With the latest target for 5k a week being the end of this quarter, it will be late 2018 at the earliest before a $35,000 version hits the roads, if not 2019.

At that time, Tesla was planning on getting to 5,000 units of production a week by the end of 2017, which meant that deliveries would start immediately after. Now, Elon seems to be saying they need 3-6 months after hitting that level to get there, meaning the original timeline was extremely optimistic. With the latest target for 5k a week being the end of this quarter, it will be late 2018 at the earliest before a $35,000 version hits the roads, if not 2019.

Demand is an obvious item, along with tax credits:

Simple economics tells us that demand increases as price decreases. While Tesla has continued to talk about being production constrained on the Model S/X, the company has basically flatlined around 25,000 units per quarter of sales for those two. With the Model 3 being less expensive, demand can obviously be higher, but we don't know what it will be like with most current versions running at $50,000 plus.

In the United States, Tesla is approaching 200,000 deliveries, which begins the clock on the phaseout of the $7,500 EV tax credit. This item is very important to many buyers, considering that it equals more than 21.4% of the base level price. InsideEvs had Tesla at almost 184,000 cumulative deliveries after April, so with a few thousand more S/X deliveries during Q2, Tesla might end up hitting the mark in Q2. The company obviously would like to hit the mark in Q3 to give more buyers access to credits, but doing that also would be a short term hit to profits and cash flow. That's not a good situation for a company with a precarious financial situation to begin with.

Making consumers wait so much longer also closes Tesla's opportunity window. The Chevy Bolt is expected to see a production increase later this year, and other competitors like the Hyundai Kona will also enter the space. Should Tesla not get the $35,000 version out until 2019 or later, it may find a lot of consumers demanding refunds and going to other vehicles.

Cost of ownership continues to rise:

I discussed this item in a previous article, but the situation has only gotten worse for those who continue to wait. Since that article, the 5-Year US Treasury rate has risen another 25 basis points to 2.90%, which means auto loan rates will continue to increase. Since Q3 2017, Tesla has already hiked its borrowing rate for consumers by 200 basis points as seen below, and I wouldn't be surprised to see another increase of 25 or 50 bps in Q3, assuming rates don't rise even further.

(Source: Tesla Model S page)

(Source: Tesla Model S page)

On a $30,000 loan, a 250 basis point increase in the rate equals about $2,000 in extra interest over a 5-year loan. That brings up the cost of the vehicle by almost 6%, and the cost goes up even more when talking about adding extra options, delivery fees, etc. For consumers that have a fixed budget for this purchase, that extra cost in interest could mean they don't add on a high margin package like Autopilot or something else.

As I mentioned in my most recent article, Tesla management has also discussed how the rise in commodity prices is hurting margins. Well, that likely means that Model 3 parts will be more expensive now, so repair costs will be higher than previously projected. Insurance for the vehicle may also be higher given Consumer Reports did not give the Model 3 a recommended mark.

Final thoughts:

Based on market share and traditional valuation metrics, Tesla shares are significantly overvalued when compared to other automakers. Investors will tell you they are long the stock for its growth potential, but the company remains well behind its target for 500,000 vehicles this year. A lot of this has to do with the $35,000 Model 3, of which there are fewer on the road today than there are Teslas floating through space. As competition heats up, the US tax credit starts to phase out, and the cost of ownership continues to rise, demand for the Model 3 will likely tail off, just like the stock has done over the past year, vastly underperforming the overall market.

(Source: Yahoo! Finance)

(Source: Yahoo! Finance)

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: Investors are always reminded that before making any investment, you should do your own proper due diligence on any name directly or indirectly mentioned in this article. Investors should also consider seeking advice from a broker or financial adviser before making any investment decisions. Any material in this article should be considered general information, and not relied on as a formal investment recommendation.