Promises and Price Tags: A Preliminary Update

Sep 22, 2016 | Budgets & Projections

The next president will enter office with the national debt at post-World War II record high levels. Debt held by the public currently totals over $14 trillion – nearly 77 percent of Gross Domestic Product (GDP) – and is projected to grow as a share of the economy to almost 86 percent by 2026 and about 150 percent by 2050. This large and growing national debt threatens to slow economic growth and is ultimately unsustainable. Yet neither presidential candidate has a plan to address it.

In June 2016, we released Promises and Price Tags: A Fiscal Guide to the 2016 Election, which estimated the budgetary impact of the policies put forward by the two major party presidential candidates – Hillary Clinton and Donald Trump. Since then, the candidates have released several new or adjusted policies.

Incorporating rough and preliminary estimates of these new policies, we find that Clinton’s plans would increase the debt by $200 billion over a decade above current law levels (compared to our prior estimate of $250 billion), and Trump’s plans would increase the debt by $5.3 trillion (compared to our prior estimate of $11.5 trillion). As a result, debt would rise to above 86 percent of GDP under Clinton and 105 percent under Trump.

Fig. 1: Debt Under Central Estimate of Candidates' Proposals (Percent of GDP)

These numbers are rough, rounded, preliminary, and based only on our central estimates (instead of the broader range we originally provided). They also exclude any economic impact and are based on our best understanding of the candidates’ policies as of September 21, 2016. We will continue to update these estimates as the campaign moves forward.

How Would Clinton's and Trump's Policies Impact the Debt?

Based on our preliminary update of our central estimates, both Clinton and Trump would increase the debt relative to current law – though Trump would increase it by an order of magnitude more, and Clinton’s plan would slightly reduce deficits if we incorporated unspecified revenue from business tax reform. Specifically, we estimate Clinton’s plans would add $200 billion to the debt over the next decade, while Trump’s plans would add $5.3 trillion.

Details of both candidates’ plans can be found in our June report Promises and Prices Tags, with updates since June available in the next section of this report.

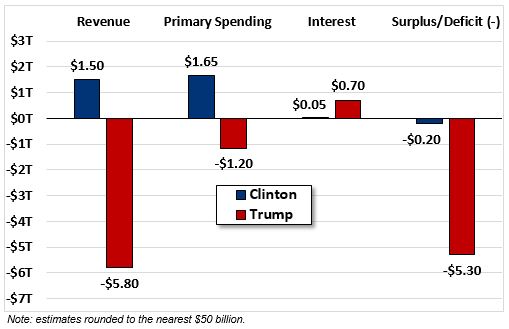

Fig. 2: Ten-Year Change in Fiscal Metrics by Candidate (Trillions of Dollars)

Clinton’s plan would increase both spending and revenue. Under our preliminary updated central estimate, she would increase primary spending by $1.65 trillion over the next decade, including about $500 billion of spending on college education, $300 billion each on paid family leave and infrastructure, and significant new health-related spending. Meanwhile, she would increase revenue by $1.5 trillion on net, including $1.05 trillion from increased income taxes on high earners and $150 billion of net business tax increases. Some of these tax changes were added to her plan just this week. Clinton’s plan would also result in roughly $50 billion of additional interest costs over a decade.

Meanwhile, Trump’s plan would decrease both non-interest spending and revenue. Under our preliminary updated central estimate, he would lose about $5.8 trillion of revenue, including $1.45 trillion from individual tax reform, $2.85 trillion from business tax reform, and $1.2 trillion from repealing the taxes imposed by the Affordable Care Act (“Obamacare”).

Trump would also reduce spending by $1.2 trillion, the net effect of almost $3.2 trillion of spending cuts – largely from the Affordable Care Act (“Obamacare”), Medicaid, and non-defense discretionary spending – and over $2 trillion of spending increases on defense, veterans, childcare, and Medicare (by reversing the “Obamacare” cuts). Under our central estimate of Trump’s plan, interest costs would increase by $700 billion over a decade.

Unfortunately, both candidates’ plans to increase the debt come on top of current law projections that already estimate that debt will grow by $9 trillion over the next decade. As a result, under Clinton’s plans debt would grow from nearly 77 percent of GDP today to over 86 percent by 2026; under Trump’s plans, debt would grow to 105 percent of GDP by 2026. This relies on conventional scoring methods and does not account for the impact of their plans on economic growth, which we will discuss in a future analysis.

Fig. 3: Estimated 10-Year Fiscal Impact of Candidates' Proposals (negative numbers add to the debt)

| Proposal | Clinton | Trump |

|---|---|---|

| Health Policies | -$0.25 trillion | -$0.05 trillion |

| Tax Policies | $1.55 trillion | -$4.50 trillion |

| Spending Policies | -$1.55 trillion | $0 trillion |

| Immigration Policies | $0.10 trillion | -$0.05 trillion |

| Subtotal, Proposals | -$0.15 trillion | -$4.60 trillion |

| Net Interest | -$0.05 trillion | -$0.70 trillion |

| Total Budgetary Impact | -$0.20 trillion | -$5.30 trillion |

| Total Debt in 2026 | -$23.30 trillion | -$28.40 trillion |

| Debt as Share of GDP in 2026 | 86% | 105% |

Note: estimates rounded to the nearest $50 billion.

These estimates are preliminary, rough, and rounded. They rely on what we know about the candidates’ plans as of September 21, 2016. In some cases, we had to rely on assumptions that may or may not materialize.

Our estimates also do not represent a pure “apples-to-apples” comparison, whereas our previous estimates did. Our tax estimates for Trump are based largely (though not entirely) on those put forward by the Tax Foundation, while our estimates of Clinton’s tax plan come in large part from the Tax Policy Center.

Furthermore, our estimates are based on conventional scoring, which does not account for the economic impact of various tax and spending changes. Some have suggested the economic effects could be large; for example, the Tax Foundation estimates Trump’s tax plan would increase GDP growth over the next decade by about 0.7 or 0.8 percent per year. However, these findings are far more generous than what official scorekeepers tend to estimate, and they do not account for the negative economic impact of higher debt, fewer immigrants, or less international trade. In our assessment, the macroeconomic impact of either candidate’s plan is likely to be small – and possibly negative – over a ten-year window.

Importantly, our analysis could change significantly based on new policies and further policy detail. We intend on continuing to update our analysis as more details are announced.

Fig. 4: Detailed Estimated 10-Year Fiscal Impact of Candidates' Proposals

(negative numbers add to the debt)

| Proposal | Clinton | Trump |

|---|---|---|

| HEALTH POLICIES | ||

| Modify the Affordable Care Act (tax and spending changes) | -$0.45 trillion | -$0.50 trillion |

| Reduce Drug Costs, Reform Insurance Markets, Expand Coverage, and Make Related Changes (tax and spending changes) |

$0.25 trillion | -$0.05 trillion |

| Increase Public Health Spending | -$0.05 trillion | n/a |

| Block Grant Medicaid | n/a | $0.50 trillion |

| Subtotal, Impact of Health Policies | -$0.25 trillion | -$0.05 trillion |

| TAX POLICIES | ||

| Reform Business Taxes | $0.15 trillion+ | -$2.85 trillion |

| Reform Individual Income Taxes | $1.05 trillion | -$0.90 trillion |

| Promote Childcare and Caretaking | -$0.15 trillion | -$0.55 trillion |

| Impose Financial Institution Fee | $0.15 trillion | n/a |

| Modify the Estate Tax and Step-Up Basis of Capital Gains at Death | $0.40 trillion | -$0.20 trillion |

| Subtotal, Impact of Tax Policies | $1.55 trillion | -$4.50 trillion` |

| SPENDING POLICIES | ||

| Increase Higher Education Spending | -$0.50 trillion | n/a |

| Support Early Education and Childcare | -$0.20 trillion | ~ |

| Increase Infrastructure Investment | -$0.30 trillion | ^ |

| Increase Defense Spending | ^ | -$0.45 trillion |

| Increase Veterans Spending | -$0.05 trillion | -$0.50 trillion |

| Enact Trade Reforms | n/a | ^ |

| Offer Paid Family Leave and Related Policies | -$0.30 trillion | -$0.05 trillion |

| Enact “Penny Plan” to Reduce Non-Defense Spending | n/a | $0.75 trillion |

| Make Other Non-Defense Changes | -$0.20 trillion | $0.25 trillion |

| Subtotal, Impact of Spending Policies | -$1.55 trillion | $0 trillion |

| IMMIGRATION POLICIES | ||

| Enact immigration reform | $0.10 trillion | -$0.05 trillion |

| Subtotal, Impact of Immigration Policies | $0.10 trillion | -$0.05 trillion |

| Subtotal, Proposals | -$0.15 trillion | -$4.60 trillion |

| Net Interest | -$0.05 trillion | -$0.70 trillion |

| Total Budgetary Impact | -$0.20 trillion+ | -$5.30 trillion` |

+ Clinton has said she would pay for her infrastructure plan as part of business tax reform. If details of this reform were released, it could generate an additional $275 billion of revenue and result in modest deficit reduction.

^ Clinton’s defense policy, Trump’s infrastructure policy, and Trump’s trade policy are all assumed to be insignificant due to current lack of detail. Once details emerge, these policies could have a significant fiscal impact. For instance, if Clinton fully repealed the sequester, it would cost $450 billion over ten years, and if Trump doubled the cost of Clinton’s infrastructure plan as he has said he would, it would cost $500 to $600 billion.

`The Trump campaign estimates its tax and regulatory plans would increase real economic growth by roughly 75 percent, from 2.0 to 3.5 percent per year. If materialized, this faster growth would generate about $3.5 trillion of additional revenue, thus reducing the cost of Trump’s policies to less than $2 trillion in total. As we’ve shown recently, however, growth rates of or even near this magnitude are extremely unlikely to materialize.

~Included under Tax Policies.

Note: Numbers may not add due to rounding.

What's New in Clinton's Plans?

Since our June report, Hillary Clinton has proposed $250 billion of 10-year spending increases, $250 billion of revenue decreases, and $550 billion of offsetting revenue increases, based on a preliminary update to our central estimate. These revenue increases have not been published on the campaign’s website but have been shared with the Committee for a Responsible Federal Budget and described on our blog.

As a result of these proposals, we now estimate Clinton’s policies will cost $200 billion over a decade, compared to $250 billion in our June estimate. Importantly, this increase could be more than offset with the business tax reform that the campaign has called for but not specified.

Fig. 5: Change in 10-Year Estimates of Clinton's Policies (negative numbers add to the debt)

| Policy | Change |

|---|---|

| June 2016 Estimate of Deficit Impact Clinton’s Policies | -$250 billion |

| Expand Access to Free Public College | -$150 billion |

| Increase Federal Health Spending | -$100 billion |

| Expand the Child Tax Credit and Offer Tax Relief for Childcare | -$150 billion |

| Simplify Small Business Taxes | -$100 billion |

| Expand the 3.8% Net Investment Income Tax (NIIT) | $250 billion |

| Further Increase the Estate Tax and Tax Capital Gains at Death | $250 billion |

| Increase the Proposed Fee on Financial Institutions | $50 billion |

| Limit Deferral on Like-Kind Exchanges | $50 billion |

| Interest Changes# | * |

| September 2106 Estimate of Deficit Impact Clinton’s Policies | -$200 billion |

#Includes debt service from new policies and changes in interest costs due to lower projected interest rates

*Indicates that this would change by less than $50 billion.

Note: Numbers may not add due to rounding.

Among the changes Clinton has proposed include (costs represent change from previous estimate):

Expand Access to Free Public College (-$150 billion). Previously, Clinton proposed “debt-free college” for low- and middle-earning families at four-year public colleges and universities in addition to completely free tuition at community colleges and various proposals to limit student loan debt. In July, she revised and expanded her debt-free college plan to work with states to offer tuition-free four-year college to students at in-state public universities if the students’ families make less than $125,000 a year (phased in over 4 years starting at $85,000). Read more about the changes to Clinton’s college plan.

Increase Federal Health Spending (-$100 billion). Previously, Clinton proposed various expansions to the Affordable Care Act (ACA), such as continued federal support for Medicaid expansion, fixing the “family glitch” to calculate health plan affordability, and limiting out-of-pocket premium costs to 8.5 percent of income. Since then, Clinton has proposed to further extend her ACA expansions by allowing individuals to buy into Medicare as early as age 55 and dedicating $40 billion over a decade to Federally Qualified Health Centers, also known as community health centers, to deliver primary care to underserved populations. Read more about these changes. She would also increase public health funding by creating a new trust fund to respond to public health emergencies, funding a comprehensive mental health agenda, expanding efforts to combat substance abuse and addiction, and tripling funding for the National Health Service Corps.

Expand the Child Tax Credit and Offer Tax Relief for Childcare (-$150 billion). Previously, Clinton set the goal of limiting childcare costs to 10 percent of family income while providing for universal preschool and expanding funding for childcare. Clinton has since expressed support for tax relief for childcare and specifically proposed to expand the $1,000-per-child Child Tax Credit to help achieve this goal. Although the Clinton campaign has not provided full details on its plan, it could reflect a proposal from Representative Rosa DeLauro (D-CT) to offer an additional $1,500 per-child refundable credit to families with children age 3 or less. Alternatively, Clinton’s plan might combine a more modest expansion of the Child Tax Credit with an expansion of the Child and Dependent Care Tax Credit such as the one proposed by President Obama.

Simplify Small Business Taxes (-$100 billion). Since our previous report, Clinton has released a detailed plan for simplifying taxes and providing relief for small businesses. Specifically, she would create a small business standard deduction and quadruple the tax credit for startup businesses. Small businesses would also be able to immediately expense up to $1 million in new investments each year, use cash accounting rather than accrual accounting, join together to form retirement plan for their employees, and claim a simplified and expanded ACA tax credit to offer health insurance in addition to other changes.

Expand the 3.8 percent Net Investment Income Tax (+$250 billion). Currently, wage income above $250,000 (for a couple) is subject to a 3.8 percent Medicare tax, while investment income above that threshold is subject to a 3.8 percent Net Investment Income Tax (NIIT). However, most income generated by owners of pass-through businesses is not subject to either tax. Clinton would apply the NIIT to income of owners of S-corporations, limited partners, and members of limited liability corporations. She would also ensure professional service businesses pay payroll taxes by preventing them from declaring certain wage income as business income. Read more about these changes.

Further Increase the Estate Tax and Tax Capital Gains at Death (+$250 billion). Previously, Clinton has proposed restoring the estate tax to 2009 levels by increasing the rate from 40 to 45 percent, reducing the exemption from $5.45 million to $3.5 million, and making other changes. According to the campaign, Clinton also supports the further increases in the estate tax proposed by Senator Bernie Sanders (I-VT) during the primary campaign – establishing a rate of 50 percent on the value of estates over $10 million, 55 percent over $50 million, and 65 percent over $500 million. In addition, Clinton would eliminate “step-up basis” of capital gains at death and thus tax the value of those gains. Although the Clinton campaign has not outlined specific parameters, it has expressed support for a variety of exemptions in order to prevent the tax from applying to taxpayers making less than $250,000 and to limit its impact on various non-financial assets such as farms, businesses, and real estate. We assume their policy would be similar to changes proposed by President Obama to tax capital gains at death. Read more about Clinton’s estate tax and step-up basis policy.

Increase the Proposed Fee on Financial Intuitions (+$50 billion). Although Clinton proposed a risk fee on banks several months ago, little detail was offered on the specifics, so we assumed a revenue impact similar to President Obama’s proposed financial institution fee. According to the campaign, however, Clinton’s proposed risk fee would be larger than what the president proposed but on a somewhat different base. Instead of a 7 basis point fee on the assets of large financial institutions, Clinton supports a sliding scale fee (based on size and risk) that averages about 13 basis points – almost twice as large as President Obama’s proposed fee. Read more about the changes to Clinton’s financial institution fee.

Limit Deferral on Like-Kind Exchanges (+$50 billion). While businesses and individuals are typically taxed on capital gains when selling property (such as real estate or artwork), no tax is imposed if property is instead traded for similar property; instead, capital gains taxes are deferred until the property is sold without being exchanged. According to the campaign, Clinton would limit these so-called “like-kind exchanges” in a manner similar to what President Obama proposed this year. That policy would limit the gains that could be deferred under like-kind exchange rules to $1 million per year while ending the use of like-kind exchanges altogether for collectibles and art. Read more about this additional offset.

Clinton’s other major policies remain similar to her June policies, described in detail in our Promises and Price Tags report.

What's New in Trump's Plans?

Since our June report, Donald Trump has proposed substantial changes and additions to his overall agenda. Most significantly, Trump has replaced his previous tax reform plan with a new one, called for repealing the defense sequester, proposed a new suite of policies to support childcare, and identified a variety of spending cuts.

Overall, our preliminary estimate finds $500 billion of new net spending cuts under our central estimate along with $4.7 trillion less in net revenue cuts, based largely on new Tax Foundation estimates.

Under our central estimate, Trump’s policies will now cost $5.3 trillion over a decade, compared to $11.5 trillion in our previous estimate, reducing the total cost of his plan in half.

Fig. 6: Change in 10-Year Estimates of Trump's Policies (negative numbers add to the debt)

| Policy | Change |

|---|---|

| June 2016 Deficit Impact of Trump’s Policies | -$11.50 trillion |

| Enact New (revised) Comprehensive Tax Reform Plan | $5.30 trillion |

| Expand Tax Breaks for Childcare and Other Caregiving | -$0.55 trillion |

| Offer Partially-Paid Maternity Leave Through Unemployment Insurance | -$0.05 trillion |

| Increase Military Spending by Repealing the Defense Sequester | -$0.45 trillion |

| Reduce Non-Defense Spending Through a “Penny Plan” | $0.75 trillion |

| Reduce Other Non-Defense Spending | $0.25 trillion |

| Interest Changes# | $1.00 trillion |

| September 2016 Estimate of Deficit Impact Trump’s Policies | -$5.30 trillion |

#Includes debt service from new policies and changes in interest costs due to lower projected interest rates.

Note: Numbers may not add due to rounding.

Among the changes Trump has proposed include (costs represent change from previous estimate):

Enact New (revised) Comprehensive Tax Reform Plan (+$5.3 trillion).1 During the primary campaign, Trump proposed a comprehensive plan to reduce individual and business taxes at a cost of roughly $9 trillion. In September 2016, Trump proposed a revised plan that the Tax Foundation estimates would cost about half as much. Like Trump’s original plan, this new plan would reduce the corporate tax rate from 35 percent to 15 percent, eliminate most business tax breaks, tax carried interest as ordinary income, impose a one-time deemed repatriation tax on profits held abroad, repeal the estate tax, and eliminate the corporate and individual Alternative Minimum Tax. Trump’s plan would also: reduce individual tax rates from 10, 15, 25, 28, 33, 35, and 39.6 to 12, 25, and 33 (previously he proposed 10, 20, and 25); expand the standard deduction from $12,600 per couple to $30,000 while eliminating personal exemptions (previously he proposed expanding the standard deduction to $50,000); cap the amount of itemized deductions a couple could take to $200,000; offer U.S. manufacturers the option of fully expensing, instead of depreciating, their equipment in exchange for giving up the deductibility of interest; and tax capital gains beyond $10 million at death in place of the estate tax. Trump has also called for measures to close the “tax gap” between taxes paid and owed.

When it comes to taxation of pass-through businesses, which pay taxes through the individual tax code, significant ambiguity remains under Trump’s plan. One interpretation is that these businesses would pay the individual tax rate of up to 33 percent; another is that they will pay the 15 percent corporate rate. A hybrid approach is also possible, for instance, if these businesses pay the corporate rate on retained profits and an additional 20 percent dividend rate on certain profits disbursed to owners as income. This ambiguity led the Tax Foundation to publish a $1.5 trillion range of estimates to reflect the policy uncertainty. Our estimates take the mid-point of this range for our central estimate, recognizing that Trump’s tax plan could cost as much as $750 billion more or less than this estimate.

Expand Tax Breaks for Childcare and Other Caregiving (-$550 billion). Since our previous report, Trump announced a comprehensive plan designed to reduce the cost of child and dependent care. On the tax side, his plan would offer an above-the-line deduction for the cost of childcare or eldercare, limited to average costs. The deduction would also be offered to stay-at-home parents and would phase out at higher incomes. Low-income families who would not benefit from the deduction would instead be offered an expanded Earned Income Tax Credit to refund half of their payroll tax burden. At the same time, Trump would allow businesses to deduct the cost of childcare benefits and expand the current tax credit for on-site childcare. Finally, Trump would allow families to establish Dependent Care Savings Accounts and contribute up to $2,000 per year tax-free. Low-income households would receive up to a 50 percent match for these contributions for the first $1,000 contributed every year.

Offer Partially-Paid Maternity Leave Through Unemployment Insurance (-$50 billion). The federal government currently requires many employers to offer 12 weeks of leave for parents of newborns but has no requirement for pay during that period. In September, Trump proposed to allow new mothers to collect up to 6 weeks of unemployment insurance over the course of their maternity leave. The campaign estimates this would cost about $2.5 billion per year and has proposed to pay for it by reducing improper payments in the unemployment insurance program; our cost estimates are similar though somewhat higher, while our savings estimates are lower (and incorporated in our estimate of reducing other non-defense spending, below).

Increase Military Spending by Repealing the Defense Sequester (-$450 billion). Since our previous report, Trump has proposed a significant increase in military spending. Specifically, he proposed to increase the number of active Army troops from 475,000 to 540,000, the number of Marine battalions from 24 to 36, the number of Navy ships from a planned 280 to 350, and the number of Air Force fighter aircraft to at least 1,200. He also proposed to modernize missile defense and cyber security and to instruct U.S. generals to present a plan to defeat ISIS. These expansions could not be paid for under the current defense discretionary spending caps. In part, Trump would pay for them by requiring other countries (including Japan, Germany, South Korea, Saudi Arabia, and members of NATO) to take more responsibility for their own defense needs or reimburse the U.S. for some of the defense provided. At the same time, he would increase the current defense caps by repealing the “defense sequester,” which reduced the caps by about $55 billion per year. Read more about Trump’s defense plan.

Reduce Non-Defense Spending Through a “Penny Plan” (+$750 billion). In order to help pay for his tax plan, Trump proposed to reduce non-defense spending by applying the “Penny Plan” to the Non-Defense Discretionary (NDD) spending caps and certain other non-defense spending. The Penny Plan reduces spending by 1 percent each year relative to the year before. Since most spending is projected to grow under current law – at least with inflation – this represents a significant cut over time. For example, applying the Penny Plan to the NDD caps would reduce the caps by 25 percent after a decade and save about $630 billion over a decade. Trump would apply the Penny Plan to certain other non-defense, non-entitlement, non-discretionary programs, which could generate modest additional savings depending on the details. Note that our total savings estimates of $750 billion is similar to – but somewhat lower than – the campaign’s $1 trillion estimate. Read more about Trump’s Penny Plan.

Reduce Other Non-Defense Spending (+$250 billion). To help pay for the cost of repealing the sequester and expanding unemployment benefits for maternity leave, Trump has proposed a number of non-defense spending cuts. Trump would accomplish this, in part, by cutting spending on programs that Congress has not formally authorized (otherwise known as unauthorized appropriations, which total over $300 billion in 2016) by 5 percent. He would also shrink the size of the federal workforce through attrition, which we assume would entail replacing federal employees at a rate of 1 for every 3 workers that retire. Finally, Trump would reduce the amount of improper and fraudulent payments for federal programs. Read more about Trump’s non-defense spending offsets.

Other Policies. In addition to the policies described above, Trump has proposed to spend $20 billion per year on school vouchers, further improve immigration enforcement, and spend more on infrastructure. However, the vouchers would come from diverting existing education funding, the immigration changes are modest relative to our prior estimates, and no official infrastructure plan has been released with enough detail to allow for or merit an estimate.

Trump’s other major policies are described in detail in our Promises and Price Tags report.

Conclusion

As in our June report, we continue to estimate that Clinton would add modestly to the debt relative to current law, while Trump would add significantly to the debt. Both Clinton and Trump have presented less costly plans, with Clinton’s plan slightly less costly than in June ($200 billion versus $250 billion), and Trump’s plan significantly less expensive ($5.3 trillion versus $11.5 trillion).

We are encouraged that Clinton continues to largely pay for her new spending and that Trump has made substantial improvements to his plan, including a less costly tax plan and new spending cuts.

Unfortunately, neither candidate has presented a proposal to address our growing national debt and put it on a more sustainable path, nor have they offered a proposal for shoring up the Social Security, Medicare, or Highway trust funds. As it currently stands, Donald Trump’s proposals would still substantially worsen the debt.

It is also disappointing that both candidates have taken large parts of the budget and tax code off the table, with both explicitly or implicitly ruling out net savings from the government’s two largest programs (Social Security and defense), Clinton ruling out revenue from anyone making less than $250,000 per year, and Trump proposing large cuts in tax revenue.

As we’ve shown before, it will be virtually impossible to put the debt on a sustainable path without changes to any of these areas of the budget or tax code; it’s also unrealistic (particularly in Trump’s case) to fix the debt with economic growth alone.

Fortunately, it is not too late for either candidate to put forward responsible policies – or modifications of their proposals – to put the debt on a more sustainable path.

We look forward to continuing to analyze their policies and working with the next president to ultimately pass the deficit-reducing tax reform, entitlement reforms, and spending changes necessary to put the budget and economy on a stronger long-term path.

Disclaimer: This paper is designed to inform the public and is not intended to express a view for or against any candidate or any specific policy proposal. Candidates’ proposals should be evaluated on a broad array of policy perspectives, including but certainly not limited to their approaches on deficits and debt.

1 Trump cites the cost of his tax plan being two-thirds offset by economic growth. In this analysis, we do not take this extra growth into account because our central estimates do not account for economic growth. In a future update of Promises and Price Tags, we will prepare a range that takes into account potential macroeconomic feedback effect.